Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

13 Appliance Tips & Hacks for Household Chores

Modern home appliances make our lives so much easier: They tackle dreaded household chores, saving us time and effort. There are lots of ways to use them, however, that you may not have thought of before. Here are 13 little-known tricks for getting more than your money’s worth from your appliances.

- Sanitize small toys and more. Use your dishwasher to wash and sanitize teething rings, small plastic toys, mouth guards, and even baseball caps. Place items on the top rack and run the dishwasher as usual with detergent (without any dirty dishes). Put smaller items in a small mesh laundry bag so that they don’t move around.

- Clean ceiling fixtures. At least once or twice a year, remove and clean your glass ceiling fixtures and light covers in an empty dishwasher. Run the machine on the normal cycle.

- Eliminate wrinkles from clothing. To smooth out wrinkled clothes or linens left too long in the dryer, toss a damp, lint-free cloth in with them. Run the load on the lowest setting for 10 to 15 minutes. Newer dryers also feature a steam setting that removes wrinkles and refreshes clothing between wears.

- Disinfect sponges and dishcloths. Kitchen sponges and dishcloths contain billions of germs. Clean and disinfect them daily by zapping them on high in the microwave for 2 minutes to kill germs.

- Freshen up your curtains. Vacuum heavy drapes with the upholstery attachment. Use the dusting brush attachment for lighter drapes. Wash sheer curtains in the washing machine on the delicate cycle, then hang them up while they’re damp to prevent wrinkles.

- Remove wax from fabric or carpet. To get rid of wax on a tablecloth, place it in your freezer until the wax is hard. Then put a flat paper bag over the wax and another under the fabric. Iron the top bag with a medium-hot iron until all the wax transfers to the bag. To remove wax from a carpet or rug, place an ice pack on the spot until the wax hardens. Shatter the wax and vacuum up the chips.

- Clean baseboards. Dusting baseboards can be a backbreaking chore. Use your vacuum cleaner and the dusting brush attachment to avoid having to bend down. Do the same to clean chair and table legs.

- Organize your fridge. Use the built-in features of your refrigerator to organize food by category. Designate certain shelves or areas for leftovers, preferably front and center, so you don’t forget they’re in there. Use special-purpose bins for their intended use: crispers for vegetables, deli trays for deli meats and cheeses, cold storage trays for meats. Newer models also feature convertible cooling zones to keep food fresh.

- Dust blinds. Extend the blinds fully and turn the slats to the closed position. Use the dusting brush attachment on your vacuum cleaner to clean the slats from top to bottom. Then open and reclose the slats in the opposite direction and repeat the process.

- Clean your microwave. The best time to clean your microwave is immediately after using it. Thanks to residual steam, all you have to do is wipe it out with a paper towel or damp sponge. To clean old messes, microwave 2 cups of water on high for 5 minutes. The steam will soften cooked-on spills, which you can wipe off with a paper towel or cloth.

- Exterminate dust mites. Dust mites live off human and animal dander and other household dust particles. They thrive in sofas, carpets, and bedding. Use the upholstery attachment to vacuum your mattress and upholstered furniture regularly to minimize dust mites. Be sure to empty the canister in an outdoor trashcan.

- Groom your pet. After you’ve groomed your dog or cat, use the dusting brush attachment to clean up after. It’s an easy way to collect shedding fur, especially from carpetted areas or upholstery.

- Remove grime from shower liners. Wash plastic shower curtain liners in the washing machine with hot water and detergent on the regular cycle. Throw in a small bath towel to help “scrub” mildew and soap scum off the liner. Then rehang the liner and let it air-dry.

Have you found any unusual cleaning hacks for your appliances? Share in the comments below!

This post originally appeared on the Windermere.com Blog

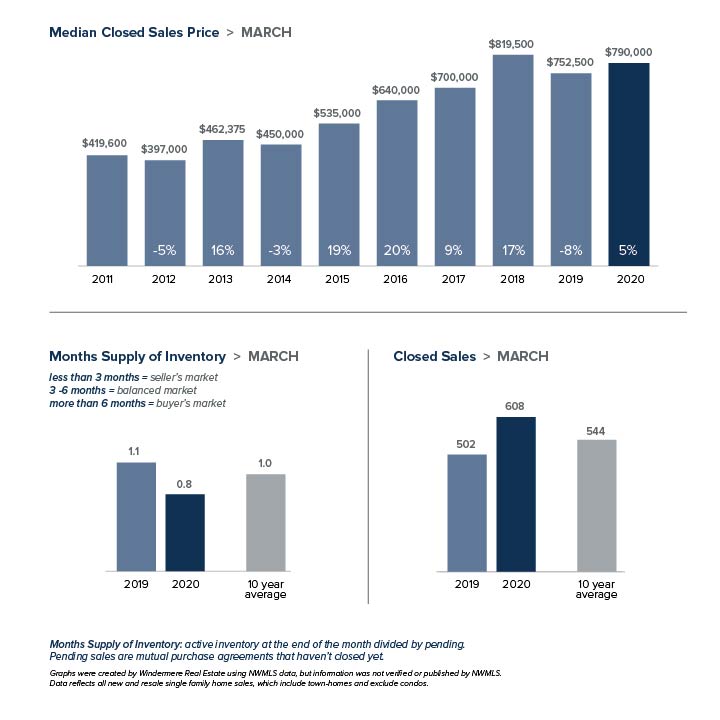

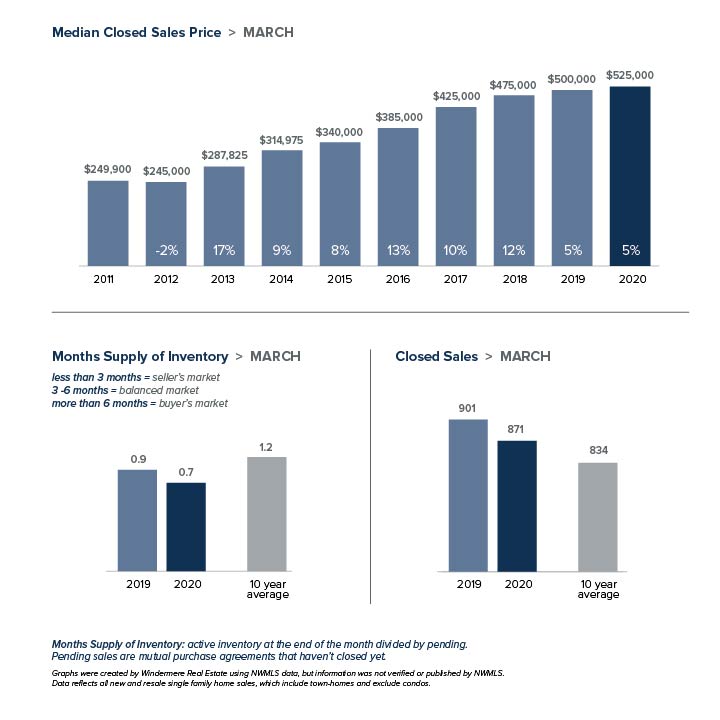

Western Washington Real Estate Market Update

The following analysis of the Western Washington real estate market is provided by Windermere Real Estate Chief Economist, Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

A MESSAGE FROM MATTHEW GARDNER

Needless to say, any discussion about the U.S. economy, state economy, or housing markets in the first quarter of this year is almost meaningless given events surrounding the COVID-19 virus.

Although you will see below data regarding housing activity in the region, many markets came close to halting transactions in March and many remain in some level of paralysis. As such, drawing conclusions from the data is almost a futile effort. I would say, though, it is my belief that the national and state housing markets were in good shape before the virus hit and will be in good shape again, once we come out on the other side. In a similar fashion, I anticipate the national and regional economies will start to thaw, and that many of the jobs lost will return with relative speed. Of course, all of these statements are wholly dependent on the country seeing a peak in new infections in the relatively near future. I stand by my contention that the housing market will survive the current economic crisis and it is likely we will resume a more normalized pattern of home sales in the second half of the year.

HOME SALES

- There were 13,378 home sales during the first quarter of 2020, a drop of only 0.2% from the same period in 2019, but 27% lower than in the final quarter of 2019.

- The number of homes for sale was 32% lower than a year ago and was also 32% lower than in the fourth quarter of 2019.

- When compared to the first quarter of 2019 sales rose in eight counties and dropped in seven. The greatest growth was in Cowlitz and Lewis counties. The largest declines were in Island and Snohomish counties.

- Pending sales — a good gauge of future closings — rose 0.7% compared to the final quarter of 2019. We can be assured that closed sales in the second quarter of this year will be lower due to COVID-19.

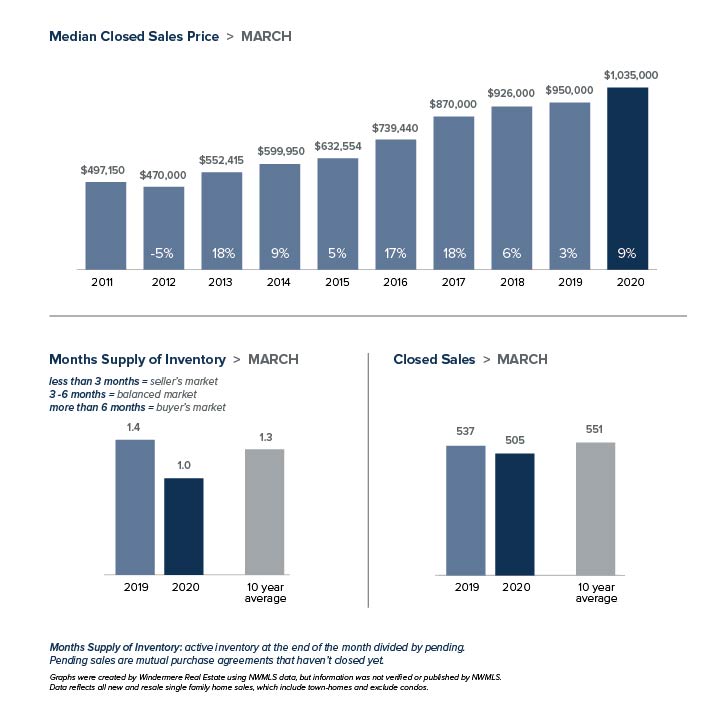

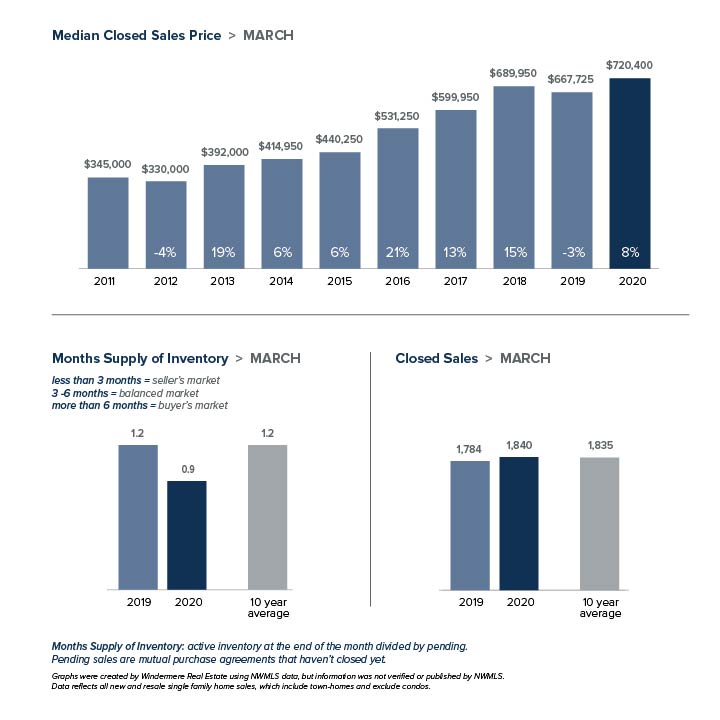

HOME PRICES

- Home-price growth in Western Washington rose compared to a year ago, with average prices up 8.7%. The average sale price in Western Washington was $524,392, and prices were 0.4% higher than in the fourth quarter of 2019.

- Home prices were higher in every county except San Juan, which is prone to significant swings in average sale prices because of its size.

- When compared to the same period a year ago, price growth was strongest in Clallam County, where home prices were up 21.7%. Double-digit price increases were also seen in Kitsap, Skagit, Mason, Thurston, and Snohomish counties.

- Affordability issues remain and, even given the current uncertain environment, I believe it is highly unlikely we will see any form of downward price pressures once the region reopens.

DAYS ON MARKET

- The average number of days it took to sell a home in the first quarter of this year dropped seven days compared to the first quarter of 2019.

- Pierce County was the tightest market in Western Washington, with homes taking an average of only 29 days to sell. All but two counties — San Juan and Clallam — saw the length of time it took to sell a home drop compared to the same period a year ago.

- Across the entire region, it took an average of 54 days to sell a home in the first quarter of the year — up 8 days compared to the fourth quarter of 2019.

- Market time remains below the long-term average across the region. This is likely to change, albeit temporarily, in the second quarter due to COVID-19.

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

Given the current economic environment, I have decided to freeze the needle in place until we see a restart in the economy. Once we have resumed “normal” economic activity, there will be a period of adjustment with regard to housing. Therefore, it is appropriate to wait until later in the year to offer my opinions about any quantitative impact the pandemic will have on the housing market.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

This post originally appeared on the Windermere.com Blog

Local Market Update – April 2020

Windermere is focused on keeping our clients and our community safe and connected. We’re all in this together. Since the early days of COVID-19, our philosophy has been “Go slow and do no harm.” While real estate has been deemed an “essential” business, we have adopted guidelines that prioritize everyone’s safety and wellness.

Like everything else in our world, real estate is not business as usual. While market statistics certainly aren’t our focus at this time, we’ve opted to include our usual monthly report for those who may be interested. A few key points:

- The monthly statistics are based on closed sales. Since closing generally takes 30 days, the statistics for March are mostly reflective of contracts signed in February, a time period largely untouched by COVID-19. The market is different today.

- We expect that inventory and sales will decline in April and May as a result of the governor’s Stay Home order.

- Despite the effects of COVID-19, the market in March was hot through mid-month. It remains to be seen if that indicates the strong market will return once the Stay Home order is lifted, or if economic changes will soften demand.

Every Monday Windermere Chief Economist Matthew Gardner provides an update regarding the impact of COVID-19 on the US economy and housing market. You can get Matthew’s latest update here.

Stay healthy and be safe. We’ll get through this together.

EASTSIDE

KING COUNTY

SEATTLE

SNOHOMISH COUNTY

VIEW FULL SNOHOMISH COUNTY REPORT

This post originally appeared on GetTheWReport.com

EMBRACE THE CHANGE

Can you believe it’s October already and Halloween is just around the corner? I love Fall (or Autumn as we call it in England!) for many reasons. October is my birthday month so what’s not to love about that. Then there’s the weather – I always have romantic hopes that there will be more crisp, cold and sunny days than dreary, rainy days.

What I love most about Fall is that it signifies change. The changing of the season, the changing of the weather, the turning back of the clocks. But there’s more to it than that. September is always our busiest month with the start of school, curriculum nights and the resuming of after school activities. So, come October, I feel we’ve all found our groove and life settles down before the Holidays – I think of it as the calm before the storm! Plus, both children have August and September birthdays so it’s a time of year when they just seem to grow up almost overnight. This year my daughter started Middle School and she’s become so much more mature in just a few short weeks. Just this morning she announced I didn’t need to walk her to the bus stop. It was bitter sweet – it was raining and only 7:15am – but I was saddened by the loss that I feel with her growing independence. My son has started 3rd grade – he’s now officially half way through his elementary school career, and I know I have just a few short years of boyhood to enjoy.

From a personal perspective, it’s at this time of year I begin to reflect back on the year. I review both my Vision Board and the Business Plan that I create in January which allows me to see not only what I’ve achieved for the year and the goals I’ve hit (or not!) but also how much life has evolved. This year, the change is more significant than in previous years. In January I challenged myself to lead a healthier lifestyle, to love and to laugh more and embrace what lay ahead held for my new family of three. I’m proud of all that has happened.

I also start planning for the year ahead. What do I want to achieve from a business perspective? Where shall we go on vacation? What personal goals shall I set myself? So far all I know is that 2019 will be the year I learn to Paddle Board and I’ll take a vacation somewhere with my parents and my brother’s family. The rest is yet to be figured out. And that’s ok. Change is what happens when you’re busy leading your life. It’s how you react to the change that counts.

Here’s to your positive changes.

Ali Tamblyn

P.S. The housing market has also experienced significant change in recent months. If you’d like to know more about the current market conditions or know anyone I can help with buying or selling a home, I’m always here to help!

Buyer’s Tips – How To Select A Buyer’s Agent

So, you’ve decided to buy a home, and now it’s time to find an agent. When buying a home the agent you choose to work with can make a huge difference – and could literally save you thousands of dollars, a ton of stress, or worst case, be the reason a transaction fails. Yet despite the high stakes, very few buyers give major consideration to who they are going to work with. The average person will take anywhere between 6-18 months before they decide to buy a home, yet they will select an agent within 24-48 hours. Most of us spend longer researching customer reviews when buying a $100 electronic appliance !

Here are my top tips for selecting a buyer’s agent:

- Ask friends and family for a referral. Personal experience is always the best barometer of what it’s really like to work with someone. But the journey shouldn’t stop there. Don’t assume that just because your great aunt Maud had a great experience with a particular agent, she’s the right agent for you. One size does not fit all – especially when it comes to real estate agents.

- Do your online research. Check out their website, Facebook pages, blogs and vlogs. If their online presence brags solely about their successes that could be a red flag. Instead, look for an agent that spends their marketing time and money educating prospective buyers about the process.

- Pick up the phone. I strongly recommend you speak to a handful of agents. How they handle that phone call will tell you a lot about how that agent works with their clients and what their priorities are. If they quickly want to take you out and view inventory before taking the time to understand your needs, it’s possible they care more about the transaction (and ultimately the paycheck) than they do about you and your buying journey.

- Meet with at least 2 agents. An in-person meeting (often referred to as a Buyer’s Interview) will tell you a lot. How do they show up, What do they ask of you in advance of a meeting, what materials have they bought with them, how do they present themselves, how much preparation have they done? If they haven’t done the prep work before they meet with a prospective client, chances are they will do even less once you commit to working with them.

- Is there Chemistry? Although this is number 5 on the list, it’s perhaps the most important. Admittedly you’re not entering a lifelong commitment with your realtor (although if he/she is a good agent you’ll want to continue working with the broker over multiple years/transactions), but you do form a very intense relationship with your broker over a very short period of time. A good agent will not just care about your ‘whats’ but also your ‘whys’. So you want to work with someone who your comfortable sharing financial, and personal information with. And believe me, a lot of personal information gets shared between buyers and agent – most of it nothing to do with houses!

- Ask questions. You want to work with an agent who is knowledgeable about, and conducted business, in your preferred areas, is familiar with your price point, works full time in the business, and can accommodate your schedule. Don’t be afraid to dig deep and get personal about their experience and work schedule.

In summary, not every agent is created equal. Take your time, do your research and go with your gut instinct. A good agent will save you money, time, stress and will be a trusted resource for many years to come – hopefully even a lifelong friend.

My next will focus on what not to look for in an agent – or rather red flags to be aware of.

When Buying A Home…Thou Shalt Not

Is it just me, or does the majority of advice we all receive about life, business, and relationships always focus on the what we should be doing? The internet is full of Top 10 things you should do if you want to…retire by the time you’re 55, lose 10 lbs, find true love, become a better you. You name it, just fill in the blank and do a google search and you’ll have a to-do list. Don’t get me wrong – I love a good to-do list just as much as the next person. In fact, as a semi type A person, I’ve even been known to write things on my to do lists even though I’ve already done them – just so I can have the satisfaction of crossi ng them off.

ng them off.

But sometimes we need to focus on the ‘to don’ts’, and never is that more important than when you’re buying a home, or in fact borrowing money for any major purchase. So in my attempt to bring some balance to the to-do vs. to-don’t equation (I am a Libra after all!) here’s my list of things you shouldn’t be doing if you are in the process of buying a home, or even considering it in the near future.

- Change jobs, become self employed, or quit your job.

- Buy or lease a new car

- Pay off your vehicle loan

- Use credit cards excessively – or more than normal. In fact a little credit card usage is a good thing, just keep it minimal

- Stop paying bills

- Spend money you have set aside for closing

- Make any major purchases – furniture, appliances etc, or in fact do anything that will originate new inquiries into your credit

- Make any large deposits without checking with your loan officer

- Change bank accounts

- Co-sign a loan for anyone

- Change marital status

Many of these may seem counter intuitive but each of the above could jeopardize your chance of receiving your mortgage – even if, in fact especially if, you’re already pre-approved and waiting to close.

So, I leave you with two words of advice. 1) Stash your Cash, and 2) If in doubt call your loan office before doing any of the above. If you’re looking for a lender, or need any further information about the home buying process continue to poke around on my website, or better yet let’s chat directly. alitamblyn@windermere.com or 425 753 1810.

THE RISKS AND PITFALLS OF USING STOCKS & SHARES TO FUND A REAL ESTATE TRANSACTION

Yesterday the stock market took a nose dive, dropping nearly 5% – one of the worst single day losses in history.

With no particular underlying reason for this volatile activity, for most of us it will have little impact, even if we have a stash of investments. The likelihood is we can ride out the losses and wait for it to regain its value. But what happens if you’re under contract to buy or sell a house, and the buyer is dependent on the sale of those assets to close on the home.? There’s a strong possibility that some the transaction could fail in such a situation.

Increasingly lenders are allowing buyers to use company shares as part of their asset/debt ratio to help increase their purchasing power. And with many Amazon and Microsoft employees who receive a healthy stock bonus every year, there are plenty of buyers in this area who do rely on those assets to fund the purchase of their house – either directly or indirectly.

Should you ever find yourself in this situation, I have two words of advice for both buyers and sellers.

- Buyers – Disclose, Disclose, Disclose! The purchase and sale agreement should specify that the closing of the transaction is dependent on the liquidation of assets and what those assets are. Also include a statement of value. Failure to do so means you don’t have a contingency in place should the value of those assets suddenly plummet overnight, even if you have a financing contingency for a loan of any sort. While some sellers may be understanding if you disclose once under contract, ultimately the seller has the right to refuse and terminate the contract. In such a hot market, where back up offers are common, is this a risk worth taking?

- Sellers –request that your buyers liquidate any such invested assets within three or five days of mutual acceptance. This should be included in the purchase and sale agreement, irrespective of how long the closing window is. Buyers, this may seem to put you at a disadvantage, but cash in the bank is always preferable to invested assets. Any appreciation you might stand to gain from those shares rising in value while you are in Escrow will be minimal compared to what you stand to lose should they drastically drop in value, and you don’t have the required cash to close on the home.

My final word of advice is for sellers working with cash buyers. While cash is great – it’s not always king. Be sure to have your realtor dig deep with the buyers agent to find out if they are really are all cash buyers, or if perhaps they are relying on the liquidation of other assets to come up with the required cash at closing. Proof of funds that reach, or better yet exceed, the value of the purchase is the best way to do this.

Don’t let the myths fool you into thinking you can’t buy

Buying a house can be scary – especially when you don’t know the facts.

If owning a home is one of your dreams, but you’ve convinced yourself you wouldn’t quality for financing, it could be time to think again. Here are the most common myths that prevent buyer’s from pursuing their home owning dreams.

Key takeaways:

Credit scores of 780 or above and 20% down payment are not key criteria. Here are the facts:

- 40% of millennials who purchased homes this year have put down less than 10%. FHA and VA loans require even less. And if either your or your partner have served in the military, you may qualify for a VA loan.

- 76.4% of loan applications were approved last month.

- The average credit score of approved loans was 724 in September.

Be thankful you don’t have your parents interest rates

I don’t know about anyone else, but following last night’s Halloween festivities, it feels like there’s not enough coffee in the world to get me going this morning. Being British, Halloween has never been a big deal for me, but as they say ‘When in Rome’. After 10 years living stateside I have to confess it’s my least favorite celebration of the year – especially as a parent. My kids are just so overexcited for so long, there’s always costume drama, it’s a late night (always fun on a week night) and then there’s the candy hangover to deal with. To say I’m feeling sluggish today is an understatement.

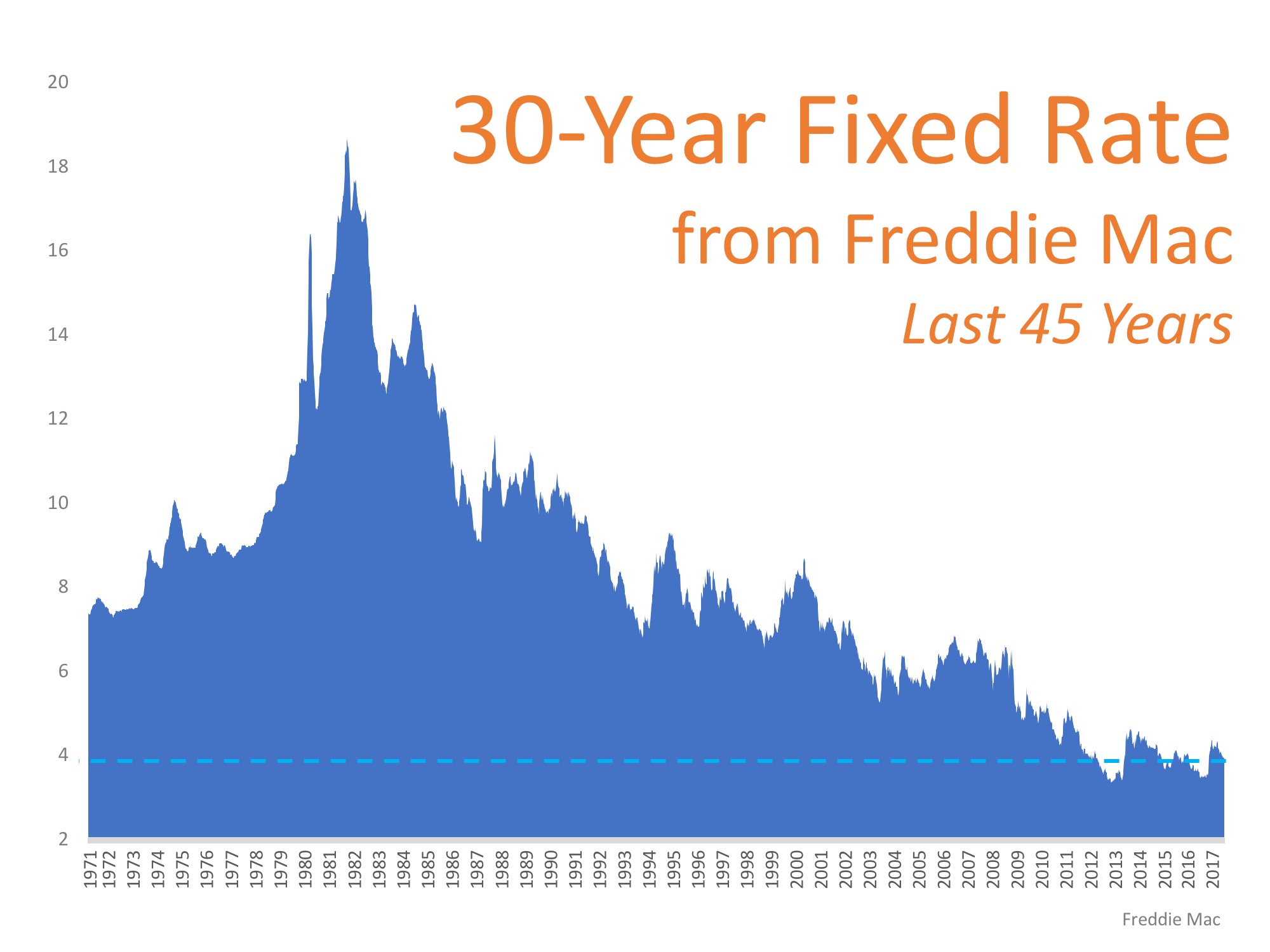

But here’s a little Hump Day Trivia that certainly shocked me – and made me oh so grateful for today’s low interest rates.

It was about this time in 1981 that interest rates reached their all time high – of a shocking 18.65%. Today’s buyers balk at it going above 4%, having seen lows in the high 3’s for much of the year. Can you imagine 18%!! Here’s some numbers that will force you throw down your left over Milky Ways in horror!

It was about this time in 1981 that interest rates reached their all time high – of a shocking 18.65%. Today’s buyers balk at it going above 4%, having seen lows in the high 3’s for much of the year. Can you imagine 18%!! Here’s some numbers that will force you throw down your left over Milky Ways in horror!

Based on today’s median house price of $853,000, and a 20% down payment, you’d be paying $10,646 per month for your mortgage. And that’s not including taxes and insurance. Add those in, and monthly payments would add up to $11,446. Wow – that’s a number I can’t even comprehend. To put it into even greater perspective: Lenders only like to see mortgage payments of approximately one third of your total net monthly income, so we’d all need to be bringing home the bacon to the tune of over $30,000 per month. It’s just not going to happen!

So while there’s much of the 80’s I’m grateful for (Madonna, George Michael and The Eurythmics to name just some of my musical heros), I very happy that we’ve not seen the interest rates that came with the wonderful music and equally shocking fashions.

Fast forward to today: As I said interest rates are currently hovering around 4%. Economists are predicting that to hold steady in the short term, but are expected a rise to closer to 5% in 2018. This has the potential of slowing down the current double digit price growth we are experiencing – which could be a good thing.